US is making Europe pay dearly for its half-hearted electrification

Europe's "small yard, big fence" moment

There is a particular quality to the panic that spreads through a continent when it realises, again, that it cannot power up its factories or fill its planes without the permission of someone who does not have its interests at heart. Europe lived that feeling in 2022. It is living it again now, in a different key. To date, the bill passed onto Europe by Trump’s war on Iran is €22bn compared with the equivalent period before the war and it’s just the begging of a mix of shock and agony. At the end of the tunnel, says an EU policy czar, awaits stagflation and secular industrial decline on a continent whose wealth depends on industry.

Across the industrial corridors of Germany and the Netherlands, energy-intensive firms that survived the Ukraine war crisis at enormous cost are running the numbers on a second shock. The hedges are shorter. The political patience of shareholders and government budget managers is close to exhaustion.The margins are thinner this time. The hair on the managers’ scalps is thinner still. As one of them told me, despairingly, “we have been struggling to stay afloat faced with China’s subsidised manufacturing and as if that were not enough, now America’s gift is a second energy crisis.. sometimes I have the feeling that the small yard, big fence” slogan of Jake Sullivan was meant for US allies. as much as it was meant for China,”

Debt levels are higher in many member states to do price intervention of the scale from 2022-2023 so some kind of joint borrowing is, yet again, on the table. Northern countries want more money more money on defense. Southern countries more for economic support to weather the looming stagflation. To top it off, from 2028, the EU must start repaying €25 billion a year on the joint debt (NextGen) taken to deal with Covid.

"The Unicorn in Captivity," tapestry, Holland, 15th century

And into that familiarity steps the crisis creator, the US petrostate, with an offer that is increasingly difficult to refuse. The kerosene tankers are there. Export terminals are running at full tilt. Contracts are ready, stretching out for twenty years, as it has been costomary from the Ukraine war onwards. Remember Germany’s SEFE with Venture Global and other suppliers, aiming to secure supply through… 2050. It won’t be any different now, if Europe wants to substitute Qatari LNG with US LNG. Except now the contracts will be priced, like bespoke suits, for a moment defined by odd levels of scarcity and risk. Belt up in petrostate dependency more snugly and for much longer than you expected or face the next few months on your own.

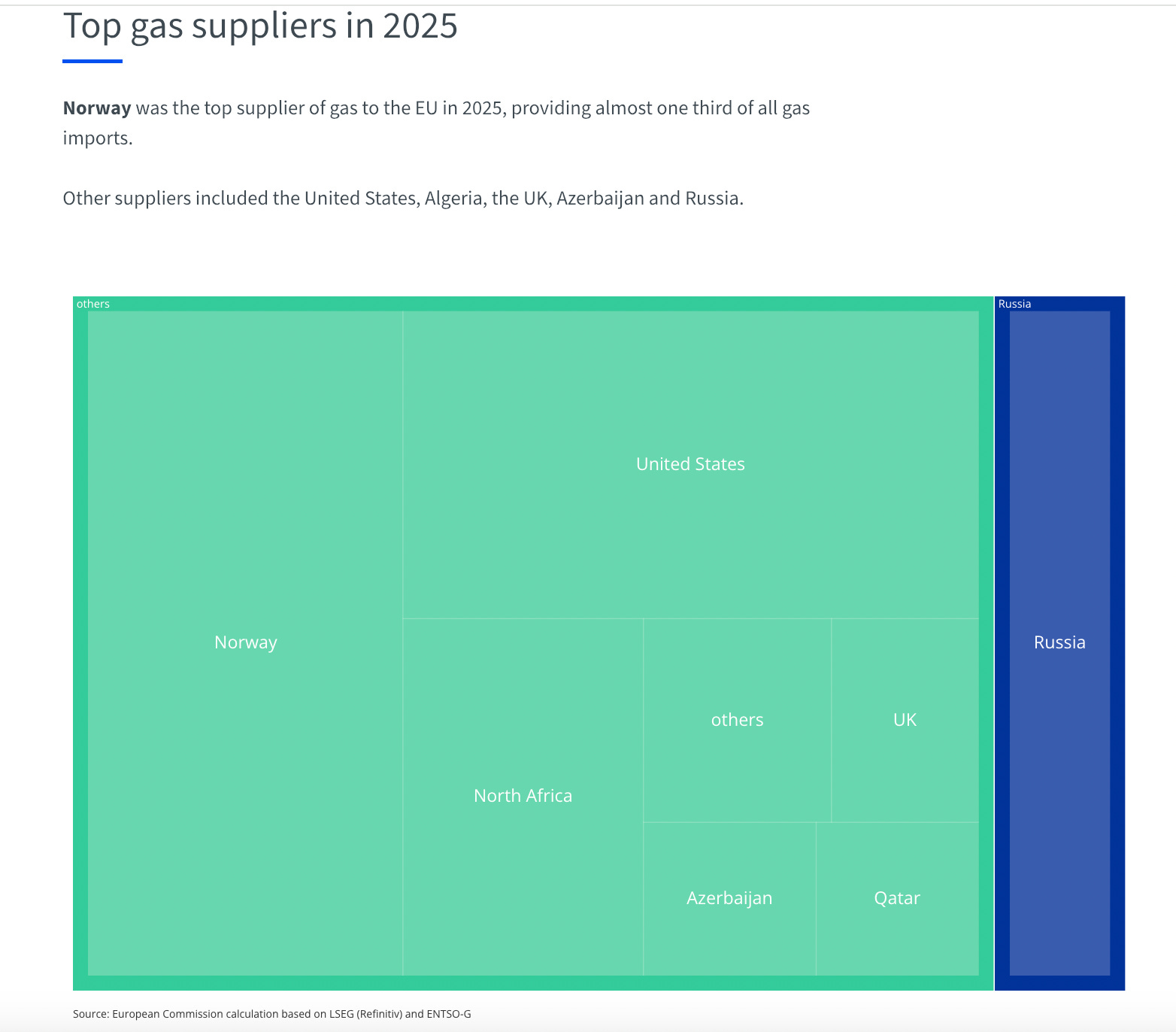

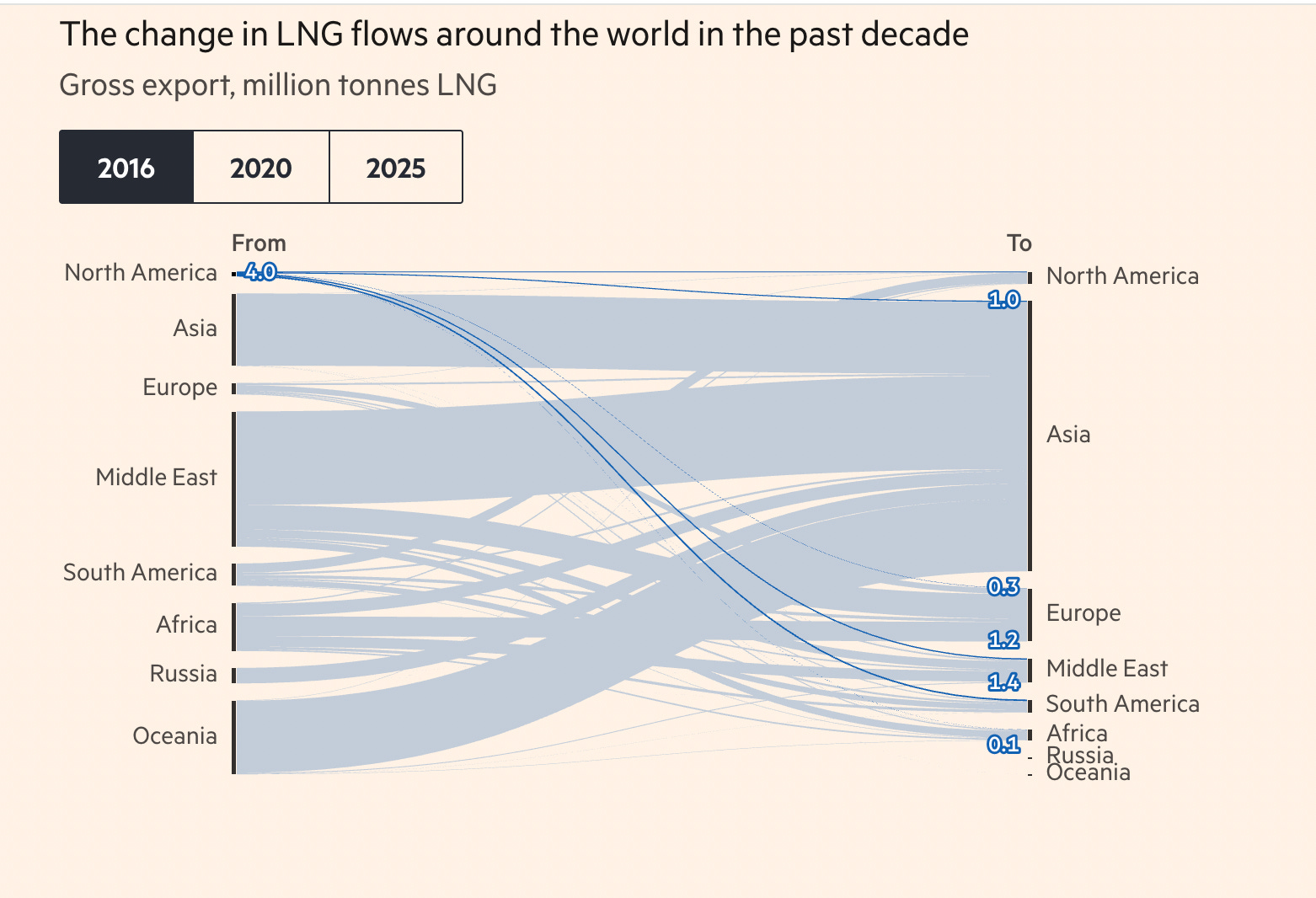

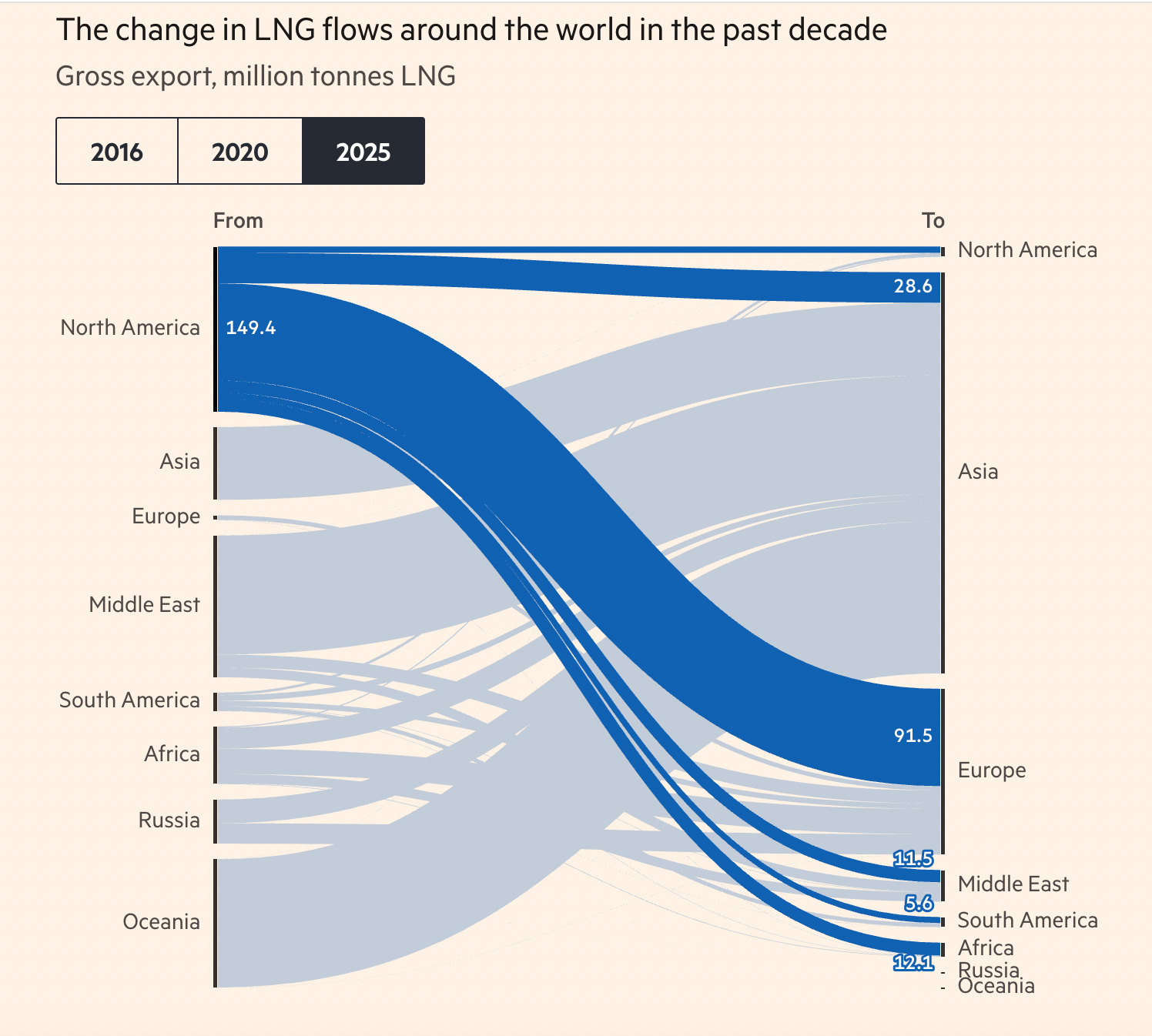

A decade ago, Europe imported almost no oil and gas from the US. Today, the European Union gets roughly half of its LNG from American exporters, alongside a growing share of crude and refined products, at a price premium, of course. This is one of the fastest energy realignments in modern history. It was not planned so much as forced. First Russia’s invasion of Ukraine, now a war leading to the closure of Hormuz. Each shock closes off one set of dependencies and pushes Europe deeper into another, throwing sand in the cogs of its once impressive manufacturing might.

Markets have already registered the shift and the dark clouds above the European growth engine, long steeped in industrial specialisations of high energy intensity. BlackRock has advised clients to underweight Europe, judging the region too exposed to energy disruptions it cannot control. And as Seb Barker of Marshall Wace put it in FT, the timelines diverge sharply. Europe needs the shock to end within weeks. The US can absorb months before its own markets begin to feel comparable strain.

The war around Iran is increasingly being read through this lens. Among its effects, it reinforces the centrality of the United States in the global energy system and the vassal nature of European and “allied” Asian economies in the world economic system. Disruption in the Gulf increases demand for alternative suppliers. The US is uniquely positioned to meet that demand. The terms on which it does so extend influence as much as they provide fuel.

This is what political economists call weaponized interdependence. The system remains interconnected, but the nodes are not equal. Some actors gain the capacity to set terms, to condition access, to turn flows into leverage. Liquefied natural gas, once framed as a flexible commodity, begins to function as a strategic asset embedded in geopolitical relationships that are US-centric in part because they are fossil energy centric.

And here is the grand strategy hypothesis: the longer the war persists, the more these contracts accumulate and extend. Infrastructure expands to support them. Financial commitments around oil and LNG harden. Even if the conflict ends and prices ease, the system does not simply revert. The contracts remain. The trade flows remain. The dependencies remain. Should the Europeans break the contracts with the great petrostate because they shift into a China gear on electrification, they will face coercion coming from defense and digital infrastructure dependence on the US. As Wes Mitchell, Trump’s former Europe hand in the State Department noted, America’s allies in Europe and Asia are stuck with the US:

“Although it is true that states tend to realign when old structures no longer serve their interests, current geopolitical realities will likely prevent a foundational realignment. In many places, including in the Indo-Pacific, U.S. partners lack an alternative anchor for regional security. And the NATO countries’ reliance on U.S. defense technology and planning ensures a degree of dependence that cannot be undone by speeches advocating greater European sovereignty. Even the EU, for all its trading might, faces real limits on how much it can strengthen its strategic ties with China. Europe’s large, inward-turning domestic market cannot absorb the goods of a fellow exporter—and vice versa. If anything, the onset of a new economic shock from China’s burgeoning overcapacity may drive the EU closer to the United States.”

This means that even with the current renewables push in many countries, the Iran war helps US fossil energy producers secure “a bigger piece of a smaller pie,” as Kingsmill Bond of Ember puts it. With Russia out of Europe’s energy mix and assuming continuing support for renewables, Europe may consume less oil and gas over time, but a larger share of what it does consume will come from the United States rather than from the Middle East.

US officials have said plainly that favourable access to liquefied natural gas is tied to broader trade alignment and no democratic debate on potential amendments to the US-EU trade treaty. What looks like a market transaction starts to function as a geopolitical interlock.

There is, of course, another, more hopeful story running in parallel.

After the 1973 oil crisis, oil’s share of global energy consumption peaked and never fully recovered. Energy shocks can force systems to change direction. After 2022, Europe accelerated the deployment of wind and solar at an unprecedented pace. Gas demand fell relative to pre-invasion levels. Electrification moved from aspiration to policy priority, supported by a growing industrial and regulatory push. On a recent visit, a European commissioner said: “The only way forward is more electrification, more nuclear, more solar, more wind, more battery capacity, more interconnectors in the European Union, and all of it with much more speed.” There is a pathway out of fossil dependence, and Europe is moving along it.

But pathways take time, and crises compress time. And when time compresses, systems do not transform. They lock in.

It did not have to be like this. Europe and China entered the 2010s chasing the same horizon, an economy rewired around electricity, but by the mid-2020s the landscape already looks uneven, tilted by scale and speed: in China, electricity now makes up roughly 30–32% of final energy use and is rising fast, while in the European Union it lingers at 24–26%, the pace slower, the momentum less certain; on the roads, the difference is even starker, China moving 11 million electric vehicles in a single year, nearly half of all new cars, Europe reaching 2.9 million but only about 24% of new sales, a transition underway yet not quite taking hold; along the rails, the contrast stretches across geography, 75% of China’s network electrified against 56% in Europe, with a high-speed system several times larger quietly pulling passengers and freight away from planes and trucks; and in the background, in the furnaces and factories where electrification is hardest, China is scaling renewable-based industrial heat faster in absolute terms, both systems still anchored in fossil fuels, but one beginning to bend more decisively toward something else.

With the Iran war, US puts a cold light on Europe’s underpowered electrification. In the absence of a fully built alternative system, fossil fuels remain the backbone of the existing one. The US know this and is working to postpone as long as possible the Europe’s chances to exit its oil and gas addiction. The US also knows European firms depend on the US market for their largest overseas revenue streams and depend on US digital infrastructures for their operations. Recently the CEO of Siemens poured cold water on talk of digital sovereignty saying such plans would bring a “disaster.” The weaponization of all this by Washington is no longer a matter of speculation and in case of a game of chicken with Washington the EU is set to lose, studies show.

So Washington does not need to prevent Europe's electrification outright. It merely needs to ensure that the transition proceeds slowly enough, and remains fragmented enough, that fossil fuel dependency endures and, with it, the deeper subordination of Europe to America’s needs.